I was struck by McCain's supposedly "bold" budget proposal to freeze non-entitlement, non-defense program spending (entitlement programs are Social Security and Medicare - and some people include Medicaid in the count, but that's not as important because Medicaid isn't nearly as big as Social Security or Medicare). WOW! What a bold plan! Let's talk a little about this "bold plan"...

Social Security and Medicare are called "entitlement programs" because once you reach age 65 you have the right to claim them. Your age is your eligibility (of course in the case of Social Security you also have to have paid into it for a certain amount of time, but it is guaranteed to everyone that paid into it). Since these programs are guaranteed, and since people are living longer, healthier lives in the United States than they used to, spending growth in these programs has been tremendous since they began. The future growth in these programs is going to dwarf even the growth to date with the retirement of the baby-boomers.

Defense spending growth hasn't been quite as continuous as entitlement program spending; it went down significantly after the Cold War in the 1990's, but obviously it makes up a nice chunk of our budget now with the War on Terror and the Iraq War.

The other thing that's grown significantly for the last several decades has been interest payments on the national debt. That's right guys, we aren't just indebted to our East Asian creditors - we need to pay them interest on top of the principle just like any other debtor. So all though McCain didn't mention it, I'll throw interest payments in, because my guess is that either Obama or McCain would cut entitlements or defense before they stop paying the interest on our debt (the world has enough doubts about our solvency... don't want to cause any more jitters)!

So, when you take all that out of the budget you have two things: what the CBO calls "other mandatory spending," and "discretionary spending". Discretionary spending includes everything from good old fashioned "bridge to nowhere" pork, to child care subsidies, to the National Science Foundation budget. That's where McCain proposes the spending freeze.

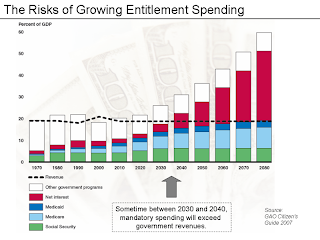

Unfortunately for McCain, he's not being as bold as he thinks he is! Non-defense, non-entitlement, non-interest payment spending has been essentially frozen for YEARS because growth in these programs has been crowded out by the growth in defense, entitlement, and interest spending! Take a look at the chart from the GAO, below, and you'll see what I mean:

OK - this is REALLY hard to see, I know - but the white bar at the top is non-entitlement spending (I believe it actually includes defense in this case!). The red, blue, and green bars are interest payments, Medicare, Medicaid, and Social Security. The dashed line is projected government revenues, and the scale for this is spending as a % of GDP. Terrible picture, I know - I tried to find a better one. But I think it illustrates my point: because of the growth in defense, entitlement, and interest spending there has been no growth in other spending anyway! The freeze is already here! In many programs, spending has actually declined already.

OK - this is REALLY hard to see, I know - but the white bar at the top is non-entitlement spending (I believe it actually includes defense in this case!). The red, blue, and green bars are interest payments, Medicare, Medicaid, and Social Security. The dashed line is projected government revenues, and the scale for this is spending as a % of GDP. Terrible picture, I know - I tried to find a better one. But I think it illustrates my point: because of the growth in defense, entitlement, and interest spending there has been no growth in other spending anyway! The freeze is already here! In many programs, spending has actually declined already.

The way to solve our long-term fiscal problem is to cut exactly what McCain proposes to let go: defense, entitlements, and interest... and we really don't have many options even there:

Defense: I'm not too excited about the prospect of cutting defense spending. Bringing a safe and responsible conclusion to the Iraq War will certainly save some money, but I agree with Obama that we're just going to have to move at least a portion of that war effort to Afghanistan. In addition, we need to reinvest in our equipment and defense infrastructure that has been worn down by Iraq, AND we need to provide a higher quality system to serve the veterans that will be returning. So I don't see much prospect of reducing defense spending, and I don't think anybody else does.

Interest: Talking about interest is easy. There are only two things to remember: first, we have to pay it - there's no choice involved. Second, the only way to reduce it is to reduce the debt. Period. [Not entirely true... we could always have our mints crank out currency which will reduce the value of our currency... then we can pay them back in worthless bills. But I don't think we want to go this route!]

Entitlements: The 800 pound gorilla in the room. The fact is, we need to cut entitlement spending or raise entitlement taxes. This isn't a debating point, it is quite simply the only way to regain fiscal responsibility. I've worked with Robert Reischauer, one of the biggest budget wonks out there, for the last two years and through him I've met lots of other big budget wonks. Doesn't matter what party they're associated with, they all agree - the solution to the budget problem is dealing with entitlement spending. Nobody owned up to this in the debate, which was telling about how hard it's going to be. Obama did mention one part of Medicare that could be cut - the Medicare Advantage "subsidy". Ever since 1997, Medicare beneficiaries have had the option of enrolling in privately administered Medicare plans, known as "Medicare Advantage". Fine - the idea was to harness the competitiveness of the private market... I can buy that. The problem is, the government ends up paying around 15% more for those plans than they do for "regular" Medicare plans. That's great - cutting that subsidy to the level of other Medicare plans and making beneficiaries pay the difference if they still want the private insurance sounds like a smart idea to me.

The problem is, even Obama didn't demand fundamental reform. I'm NOT an expert on entitlement programs, but even I could suggest:

- First and foremost, freezing physician payments which is one of the fastest growing components of Medicare.

- Raise the eligibility age for both programs

- Eliminate the FICA tax cap. I'm not sure exactly what it is now, but it's somewhere around $100,000. You have to pay something like 7.5% of your taxable income into Social Security up to $100,000 right now. After $100,000, your income isn't taxed!!! Why is this? This means that the rich actually pay a LOWER tax rate than the poor when it comes to Social Security! Now, I know there are legitimate ethical cases against a progressive income tax... but who in their right minds supports a REGRESSIVE tax??? Raising or eliminating this cap would help things out.

- Cut benefits. Yes - my specific suggestions and expertise end here, and I have to offer the non-descript "cut benefits". Someone more familiar with the program than I can get into the specifics.

We can do this - we need to have the strength to take on the entitlement programs. That will make substantially more difference than any pork-cutting programs that McCain and Obama propose. Nobody embraced this, although Obama made it clear that he was open to reducing some entitlements. I hope he's just holding his tongue because saying "I'm going to cut Social Security" would be the kiss of death on the campaign trail. Perhaps he'll be more energetic on this front than he lead on. But don't be fooled by that little discussion they had on the budget... McCain wasn't being bold at all - he was essentially describing the status quo. And Obama didn't offer a whole lot either.

{kind=link}