I stumbled across a very interesting article from 1992 by our current Fed Chairman, Ben Bernanke: http://fraser.stlouisfed.org/docs/MeltzerPDFs/bernon83.pdf

In it, he discusses what is essentially a transaction cost approach to the Great Depression - arguing that uncertainty about borrowers substantially raised the "cost of credit intermediation". A scary proposition, because we are certainly facing these types of problems now... Senate Republicans themselves have bemoaned it.

Friday, December 19, 2008

Tuesday, November 25, 2008

Next Research Project

OK - so details still need to be worked out, but I am ready to jump into my next research project, now that my presentation at the Southern Economic Association is over. I think my next research project will deal with worker flows and job flows - I'll be inserting myself into the world of economists like John Haltiwanger (Maryland), Robert Shimer (Chicago), and Robert Hall (Stanford) (each of these guys are really well respected - Haltiwanger and Shimer both have awesome websites with great data made publicly available). This research will also get me some real experience with macroeconomics, without leaving labor economics. Unemployment and job churning is really an interesting area because it's one of the few areas where labor economics (a traditionally "micro" endeavor) and macroeconomics meet. Anyway, I hope gaining some experience here can help set me up to go on and study labor and macro at University of Maryland, which would be a great academic background to have in an economics career.

Worker flow and job flow research emerges out of the idea that unemployment statistics mask underlying dynamics in the labor market. For example - the most recent unemployment rate was 6.5 percent (up from 6.1 percent in September). 6.5 percent of the people in the labor force were out of work in October, 2008. But what does this mean? It could mean that the hiring rate in October was zero and the separation rate was 0.4 percent (6.1 percent in September increases to 6.5 percent because 0.4 percent of the labor force lost jobs, and none gained). In reality, this isn't how it works. The hiring rate might be 7.3 percent, and the separation rate might be 7.7 percent, causing the net unemployment rate to increase by 0.4 percent. Or "churning" could be even greater - hiring could be at 11.2 percent, and the separation rate could be at 11.6 percent! You get the idea. Understanding these underlying dynamics that contribute to our snap-shot pictures of unemployment can go a long way toward diagnosing underlying problems, understanding issues in productivity growth, understanding the effect of different labor market institutions, etc.

Hiring and separation are "worker flow" concepts. Workers "do" those things. Another way of conceiving of the problem is with "job flows". If all firms employ the same amount of workers and the labor force does not grow, the unemployment rate should stay the same. However, if firms lower their employment levels (job destruction) or raise their employment levels (job creation), then unemployment will change. The distinction between these job flows and the worker flows that I mentioned earlier is important. Job flows can be thought of as a subset of worker flows. A worker flow (a hiring or separation) doesn't necessarily imply a job flow, as long as the worker who separated from his job is replaced, and the worker who was hired is replacing an old worker. However, net worker flows and net job flows have to be equal. A standard statement of this is:

Net change in employment = Hires - Separations = Job Creation - Job Destruction

There have been a few "accepted facts" that have been established for worker flows and job flows, and their relationship to unemployment - at least for the national economy:

1. Robert Hall, who primarily deals with worker flows, has established that recessions are caused by declines in the hiring rate, not by spikes in the separation rate (as is commonly thought). He also demonstrates that we shouldn't expect to see separation rates change in response to productivity shocks, and that if we do it is a sign of inefficient wage bargaining (he specifically attributes it to unionization).

2. Haltiwanger and his colleages, who primarily deal with job flows, have established that recessions are caused by spikes in the job destruction rate, and not by an increase in job creation.

These "facts" seem to contradict each other, but they don't have to. Job destruction does not equal separation and job creation does not equal hiring. But they do have different policy implications. Obama has proposed a job creation tax credit. Others propose public employment measures, and others propose cuts in the capital gains tax. There is new legislation in Congress to strengthen unionionization, which as Hall demonstrates - has major implications for separation rates. In other words - this line of research directly connects my labor interests to macroeconomics, and it has LOTS of very relevant "policy levers" to talk about.

The task that interests me most right now is looking at worker flows, job flows, and their relationship to unemployment at the local level. The Census Bureau has quarterly data on job flows and worker flows at the county level for many states - the mid-Atlantic region (I'm thinking of Pennsylvania, New Jersey, Delaware, Maryland, West Virginia, and Virginia) have data going back to before the 2001 recession. I'm interested in tracking the relationship between job and worker flows and unemployment for each county over this period, to ascertain whether Hall and Haltiwanger's "facts" hold true at the level of the local economy. I then want to look into what predicts cases where these "facts" don't hold true, to see if it will help explain the abysmally high unemployment rates in West Virginia, but unbelievably low unemployment rates in Northern Virginia and parts of Maryland. Could it be that the underlying relationship between job flows, worker flows, and unemployment is different in these areas? What implications would this have for policy?

Who knows where this will take me. What's exciting about this field is that new, better data is coming out all the time, and the data is very very accessible.

I think this will be one of two major "research planks" I will try to develop before grad school. The other is research on skilled labor and science and tech policy issues. I don't want to just be a "labor guy". I want to be more forward looking and I want to consider national competitiveness issues as well. A lot of this will come from migrating into some more macroeconomic topics - but I think emphasizing skilled labor and the economics of science and technology will help shape that research agenda as well. I think if I build up a resume with "economic nationalism" papers and presentations it will make admissions departments much more wary than if I have "job flows" papers and presentations - so I figure this is the stuff to work on now. I'll keep reading and thinking about everything, obviously.

Time to search for new calls for papers!

Monday, November 10, 2008

The Ghosts of Keynes and FDR

After spending decades in exile, people can't seem to shut up about John Maynard Keynes and FDR now. Paul Krugman (Princeton professor, NYT columnist, professional Bush-basher, and the most recent Nobel laureate in economics) is on a deficit spending bender on his blog,

here: http://krugman.blogs.nytimes.com/2008/11/10/fiscal-fdr/

here: http://krugman.blogs.nytimes.com/2008/11/08/new-deal-economics/

and here: http://krugman.blogs.nytimes.com/2008/11/08/stupid-fiscal-tricks/

Expect more of this as the pundits mull over the meaning of Obama's Friday press conference and his meeting today at the White House - and as they digest aid to the auto industry, new aid to AIG, and the massive stimulus package that China just passed.

I think this is good and bad. It's good because everything is on the table for the first time in a long-time. When the worst-case scenario is full-scale economic collapse, you don't want to rely solely on the solutions that were vetted by Barry Goldwater. It's bad because in our frenzy to respond to the recession we may exascerbate other "pre-existing conditions" - a $10.5 trillion dollar national debt with a deficit that may top $1 trillion in the first year of the Obama administration, coupled with wary international investors and growing entitlement spending. Krugman and a lot of the Keynesian crowd have been very cavalier towards deficit hawks in the last several weeks.

Their argument is disappointingly shallow: "bank failures are a real problem right now - the so called Treasury bubble is a theoretical problem projected to happen some time in the future". Their new-found confidence in deficit spending is good, in my mind, but their embrace of all deficits, no matter what the size or projected future cost, is disturbing. Moreover, Congressional Democrats may be emboldened by a Nobel laureate stamp of approval on massive spending increases.

Here's what we need to do - pick up the "General Theory of Employment, Interest, and Money", and reread it before we jump into anything. I did this last year and it looks like it would probably be smart to reread it again before January. The focus of the General Theory was productive employment and investment that would sustain employment temporarily, AND lay the foundation of an economic recovery. Keynes ridiculed politicians who were more than willing to pay unemployed workers to do nothing but balked at the idea of paying them to build public works that would speed an economic recovery. He also spent a lot more time talking about state management of investment than he did talking about state management of consumption. These sound like details, but it makes a big difference.

We probably do need to extend unemployment insurance - but before there's too much talk about expanding Medicaid or welfare or Medicare we need to instead consider grants to states that are now slashing transportation projects and teacher payrolls. If we hand out twice as many foodstamps as we did before, we're just going to relieve some of the pressure on family budgets and subsidize the food industry - but if we build new bridges and roads we relieve pressure on family budgets while at the same time setting a foundation for more robust economic growth to occur several years down the line. Same with "green-collar jobs" - now is the time for the government to start pilot programs in wind and solar energy that can relieve pressure on family budgets, but also position private enterprise to move into these areas when they become less skiddish about investing than they are now.

Keynes was right. Everybody accepts the basic Keynesian logic now (it's why Bush cut taxes in 2001, after all). But re-embracing Keynes and FDR doesn't mean you drive the country further into debt with whatever politically popular program you want. People like Paul Krugman need to reread what Keynes actually said before criticizing budget hawks like David Walker. Any progress we make with untargeted spending may unravel if the debt doubles again under Obama, like it did under George "Borrow and Spend" Bush.

Relevant Links:

On investing in American infrastructure -

1. http://www.brookings.edu/events/2008/0725_infrastructure.aspx

2. http://www.newamerica.net/programs/economic_growth/infrastructure#

On the real Keynes -

1. http://www.levy.org/vdoc.aspx?docid=1082

Crisis of 2008 News Referenced in this Note -

1. http://www.washingtonpost.com/wp-dyn/content/article/2008/11/10/AR2008111000502.html?hpid=topnews

2. http://www.washingtonpost.com/wp-dyn/content/article/2008/11/09/AR2008110900701.html?hpid=topnews

3. http://www.politico.com/news/stories/1108/15426.html

An Interesting New FDR Book That Someone Who Loves Me Oughta Get Me for Christmas -

1. http://www.amazon.com/Traitor-His-Class-Privileged-Presidency/dp/0385519583/ref=pd_bbs_sr_1?ie=UTF8&s=books&qid=1226329466&sr=8-1

here: http://krugman.blogs.nytimes.com/2008/11/10/fiscal-fdr/

here: http://krugman.blogs.nytimes.com/2008/11/08/new-deal-economics/

and here: http://krugman.blogs.nytimes.com/2008/11/08/stupid-fiscal-tricks/

Expect more of this as the pundits mull over the meaning of Obama's Friday press conference and his meeting today at the White House - and as they digest aid to the auto industry, new aid to AIG, and the massive stimulus package that China just passed.

I think this is good and bad. It's good because everything is on the table for the first time in a long-time. When the worst-case scenario is full-scale economic collapse, you don't want to rely solely on the solutions that were vetted by Barry Goldwater. It's bad because in our frenzy to respond to the recession we may exascerbate other "pre-existing conditions" - a $10.5 trillion dollar national debt with a deficit that may top $1 trillion in the first year of the Obama administration, coupled with wary international investors and growing entitlement spending. Krugman and a lot of the Keynesian crowd have been very cavalier towards deficit hawks in the last several weeks.

Their argument is disappointingly shallow: "bank failures are a real problem right now - the so called Treasury bubble is a theoretical problem projected to happen some time in the future". Their new-found confidence in deficit spending is good, in my mind, but their embrace of all deficits, no matter what the size or projected future cost, is disturbing. Moreover, Congressional Democrats may be emboldened by a Nobel laureate stamp of approval on massive spending increases.

Here's what we need to do - pick up the "General Theory of Employment, Interest, and Money", and reread it before we jump into anything. I did this last year and it looks like it would probably be smart to reread it again before January. The focus of the General Theory was productive employment and investment that would sustain employment temporarily, AND lay the foundation of an economic recovery. Keynes ridiculed politicians who were more than willing to pay unemployed workers to do nothing but balked at the idea of paying them to build public works that would speed an economic recovery. He also spent a lot more time talking about state management of investment than he did talking about state management of consumption. These sound like details, but it makes a big difference.

We probably do need to extend unemployment insurance - but before there's too much talk about expanding Medicaid or welfare or Medicare we need to instead consider grants to states that are now slashing transportation projects and teacher payrolls. If we hand out twice as many foodstamps as we did before, we're just going to relieve some of the pressure on family budgets and subsidize the food industry - but if we build new bridges and roads we relieve pressure on family budgets while at the same time setting a foundation for more robust economic growth to occur several years down the line. Same with "green-collar jobs" - now is the time for the government to start pilot programs in wind and solar energy that can relieve pressure on family budgets, but also position private enterprise to move into these areas when they become less skiddish about investing than they are now.

Keynes was right. Everybody accepts the basic Keynesian logic now (it's why Bush cut taxes in 2001, after all). But re-embracing Keynes and FDR doesn't mean you drive the country further into debt with whatever politically popular program you want. People like Paul Krugman need to reread what Keynes actually said before criticizing budget hawks like David Walker. Any progress we make with untargeted spending may unravel if the debt doubles again under Obama, like it did under George "Borrow and Spend" Bush.

Relevant Links:

On investing in American infrastructure -

1. http://www.brookings.edu/events/2008/0725_infrastructure.aspx

2. http://www.newamerica.net/programs/economic_growth/infrastructure#

On the real Keynes -

1. http://www.levy.org/vdoc.aspx?docid=1082

Crisis of 2008 News Referenced in this Note -

1. http://www.washingtonpost.com/wp-dyn/content/article/2008/11/10/AR2008111000502.html?hpid=topnews

2. http://www.washingtonpost.com/wp-dyn/content/article/2008/11/09/AR2008110900701.html?hpid=topnews

3. http://www.politico.com/news/stories/1108/15426.html

An Interesting New FDR Book That Someone Who Loves Me Oughta Get Me for Christmas -

1. http://www.amazon.com/Traitor-His-Class-Privileged-Presidency/dp/0385519583/ref=pd_bbs_sr_1?ie=UTF8&s=books&qid=1226329466&sr=8-1

Friday, November 7, 2008

Daniel's Cabinet Advice

-Treasury - Tim Geithner

-State - Bill Richardson

-Defense - Gates for at least six months, then Wesley Clark (this isn't nearly as essential as people think it is, except for appearances. And appearances can mean a lot. We have to remove ourselves from Iraq safely, and one way to do it safely is to not do it abruptly).

-NSA - Richard Lugar (in 1991 he and Sam Nunn demonstrated that they understood the real post-Cold War threats that America faced by passing a landmark non-proliferation bill. Perfect guy to advise Obama on national security threats. Nunn would have been good too, but Lugar is a Republican and it would be nice to have a bipartisan cabinet. Plus he's from Indiana, and it would be great to flatter the Hoosiers and keep Indiana blue).

-Education - Joel Klein?!?!?! (repeating reasonable sounding buzz on this one)

-CEA Chair - Paul Krugman (he is "shrill", but he's incredibly intelligent and probably the most believable Keynesians around - he'll be a nice counterweight to the "neoliberals" that will have Obama's ear - Rubin, Summers, et al.)

-Labor - Robert Reich (eh)

-Health and Human Services - Robert Reischauer (intelligent budget hawk, and my boss... perfect guy to reign in Medicare - experience at CBO and MedPac)

-Transportation - Tim Kaine (could really energize the nation to get some major public infrastructure investments underway)

-Ambassador to the UN - Bill Clinton (I don't know why people suggest Colin Powell for this. I love the guy, but his darkest moment, in my mind, was at the UN. We don't want to send him back there and remind people).

-State - Bill Richardson

-Defense - Gates for at least six months, then Wesley Clark (this isn't nearly as essential as people think it is, except for appearances. And appearances can mean a lot. We have to remove ourselves from Iraq safely, and one way to do it safely is to not do it abruptly).

-NSA - Richard Lugar (in 1991 he and Sam Nunn demonstrated that they understood the real post-Cold War threats that America faced by passing a landmark non-proliferation bill. Perfect guy to advise Obama on national security threats. Nunn would have been good too, but Lugar is a Republican and it would be nice to have a bipartisan cabinet. Plus he's from Indiana, and it would be great to flatter the Hoosiers and keep Indiana blue).

-Education - Joel Klein?!?!?! (repeating reasonable sounding buzz on this one)

-CEA Chair - Paul Krugman (he is "shrill", but he's incredibly intelligent and probably the most believable Keynesians around - he'll be a nice counterweight to the "neoliberals" that will have Obama's ear - Rubin, Summers, et al.)

-Labor - Robert Reich (eh)

-Health and Human Services - Robert Reischauer (intelligent budget hawk, and my boss... perfect guy to reign in Medicare - experience at CBO and MedPac)

-Transportation - Tim Kaine (could really energize the nation to get some major public infrastructure investments underway)

-Ambassador to the UN - Bill Clinton (I don't know why people suggest Colin Powell for this. I love the guy, but his darkest moment, in my mind, was at the UN. We don't want to send him back there and remind people).

Tuesday, October 28, 2008

Please Remember What It Means to Be An American This Week

For reasons that won't be enumerated here, my hearts been hanging a little heavy lately. Between the election, the wars, and the economic crisis, stress is high for everyone in this country. I guess since I haven't posted for awhile - and since I might not post again until after the election - I wanted to make an appeal for people to think hard about and remember what it means to be an American.

It doesn't mean you ascribe to a particular political party or ideology. It doesn't mean you ascribe to a particular religion. You don't have to come from a small town to be an American, or a big city. You don't have to be a soldier or a farmer either - although many of the world's soldiers and farmers are Americans. You can be sexually attracted to someone of the same sex and still be an American. You don't have to have light skin to be an American. And for all the serious and important debate about the bureaucratic process of becoming a citizen, it's not important at all to have been born here for you to be an American. You can have an abortion and still be an American. You can commit a crime and still be an American.

I tried a couple "what does it mean to be an American?" paragraphs to tack on here, and I can't seem to write one that makes sense. I just know that in America, individuals matter - not groups that individuals may belong to.

Monday, October 13, 2008

Krugman Wins Nobel Prize in Economics

Paul Krugman, renowned trade economist at Princeton University and regular columnist for the New York Times, won the Nobel Prize in Economics this morning for his work on economies of scale and its effect on trade patterns and the location of economic activity. This is bread and butter Krugman, of course - but the announcement also noted his role as an "opinion maker" through his books and his writing for the New York Times.

This should be an interesting platform for Krugman to continue to discuss the financial crisis and the bailout, which he has had some very strong opinions on.

Congratulations Paul! This is very, very well deserved.

This should be an interesting platform for Krugman to continue to discuss the financial crisis and the bailout, which he has had some very strong opinions on.

Congratulations Paul! This is very, very well deserved.

Tuesday, October 7, 2008

Krugman, the crisis, and the late 1990s

During the late 1990s - the halcyon days of the Clinton administration and the tech boom - were disastrous for many middling economies: Mexico, South Korea, Japan, Russia, Brazil, Indonesia, Thailand, etc. Throughout this second tier of global economic powers, currencies failed, governments defaulted on their debts, and bank runs on the order of our Great Depression occured. A lot of people missed it because of how well the U.S. was doing - but it was a milestone event in international finance that directly threatened the prospects of economic globalization.

Part of the reason for this was the irresponsibility of central banks in these countries. That's why it wasn't just businesses that failed - currencies and national treasuries failed.

Krugman points out that right now the Federal Reserve board is doing one of the irresponsible things that these second tier economies were criticized for back in the late 1990s - putting a lot of corporate securities on their balance sheet. This is happening at a time when the U.S. government is already leveraged to the hilt - trillions of dollars in debt to international investors. This is a very very dangerous situation to be in. This is how a violent rebalancing of international financial imbalances happens.

I agree with Krugman - we needed to do something and the bailout bill as it stands is better than nothing. But we can't stop their and we cannot throw responsibility out the window at the Federal Reserve to stabilize things in the short-run.

The scariest thing is we're in uncharted territory. When has a superpower's currency crashed and defaulted on it's debt? I don't know of an occassion personally (although I don't know much about macroeconomic history). I know of superpowers being surpassed, but not crashing (USSR doesn't count... I consider them a faux-superpower because their power was based on nuclear weapons and perception - not solid strength). So is this all likely? I have no freaking clue... but I really don't like our central bankers taking a page out of the 1996 playbook of central bankers in Russia, South Korea, or Indonesia.

Part of the reason for this was the irresponsibility of central banks in these countries. That's why it wasn't just businesses that failed - currencies and national treasuries failed.

Krugman points out that right now the Federal Reserve board is doing one of the irresponsible things that these second tier economies were criticized for back in the late 1990s - putting a lot of corporate securities on their balance sheet. This is happening at a time when the U.S. government is already leveraged to the hilt - trillions of dollars in debt to international investors. This is a very very dangerous situation to be in. This is how a violent rebalancing of international financial imbalances happens.

I agree with Krugman - we needed to do something and the bailout bill as it stands is better than nothing. But we can't stop their and we cannot throw responsibility out the window at the Federal Reserve to stabilize things in the short-run.

The scariest thing is we're in uncharted territory. When has a superpower's currency crashed and defaulted on it's debt? I don't know of an occassion personally (although I don't know much about macroeconomic history). I know of superpowers being surpassed, but not crashing (USSR doesn't count... I consider them a faux-superpower because their power was based on nuclear weapons and perception - not solid strength). So is this all likely? I have no freaking clue... but I really don't like our central bankers taking a page out of the 1996 playbook of central bankers in Russia, South Korea, or Indonesia.

Updates...

Wow - it's been over a week since I last posted. And this one will have to be concerned with a few media updates.

First, the crisis is spreading despite the eventual passage of the bailout bill. Would it have helped if the Treasury could have got the ball rolling last Monday instead of last Friday? Since most of the global markets tanked this weekend, it probably would have... but we'll never really know.

More disconcerting is that it's starting to move into the "real economy" - losses aren't cropping up just on paper anymore - they're affecting auto sales. It makes sense that this is next - cars are the next biggest consumer product purchased on credit after houses (which are already doing crappy as everyone already knows). This move into the "real economy" is bad. People have been talking about how this crisis is nothing like the Great Depression because "the fundamentals" - unemployment, GDP growth, etc. - are still strong. Here's the problem with that logic: people have this idea that the bottom fell out in the recession all at once in 1929. It didn't! The stock market crashed in 1929, but GDP growth didn't reach it's low point and unemployment didn't reach it's high point until several years later, in the early 1930s. The fact that the crisis so far has been restricted to the housing market and the money market is no proof that "the rest of us are safe". This drop in auto sales is likely an opening salvo in a war on the "real economy" - and we're probably going to start to see other bad numbers trickle in.

The biggest recent news is that the crisis is spreading to Europe and Asia. This is also bad news in terms of the possibility of a broader recession. The only thing buoying us in the last year or so has been - ironically - our exports. If aggregate demand contracts in Europe and Asia, you can bet that component of GDP is going to drop and suddenly we're going to be looking at negative GDP growth - recession territory. Paul Krugman has a good, albeit brief post on the global nature of the crisis this morning. He specifically compares out situation to that of Brazil, Thailand, Indonesia, Russia, and South Korea - who crashed in 1997-1998, in part because of their high exposure international financial flows. These have increased in the U.S. dramatically since 1995 or so. Which begs the question - what is the end game here? I see two things that could potentially happen - first, we could close up and insulate ourselves from the world economy. It could also be a Bretton Woods moment - since we know that all this international connectivity exposes us to substantially more financial risk than in the past, it may be appropriate not just to reregulate our own financiers - but to establish a new international regulation of financial markets on the ruins of Bretton Woods. Not that we've been hearing any clamoring for this... and besides - who could possibly stand in for Keynes?

In election news... well, Obama is giving McCain a whooping for the most part. A few concerns - Palin is performing better than she has been (could she really be performing worse???), and McCain is on a smear hyper-campaign right now. I think it will make him look childish - but you never know. But overall I think it looks good. Michigan is a lock - Ohio, Pennsylvania, and Virginia are leaning Obama. Florida still sounds tough, but if Obama really gets all those swing states perhaps we could do without. I hear McCain and Obama are now heating up the war over Nebraska!... NEBRASKA! McCain is on the defensive in traditional red states. Not only does this not bode well for him in the red states, it means it's that much less resources he's going to spend in the blue states and the swing states - which is going to make keeping Michigan, Ohio, Pennsylvania, Virginia, etc. that much easier for Obama. Good news all around.

And... as I've been updating for months... Gilmore is a lost cause. Go Warner!!!

First, the crisis is spreading despite the eventual passage of the bailout bill. Would it have helped if the Treasury could have got the ball rolling last Monday instead of last Friday? Since most of the global markets tanked this weekend, it probably would have... but we'll never really know.

More disconcerting is that it's starting to move into the "real economy" - losses aren't cropping up just on paper anymore - they're affecting auto sales. It makes sense that this is next - cars are the next biggest consumer product purchased on credit after houses (which are already doing crappy as everyone already knows). This move into the "real economy" is bad. People have been talking about how this crisis is nothing like the Great Depression because "the fundamentals" - unemployment, GDP growth, etc. - are still strong. Here's the problem with that logic: people have this idea that the bottom fell out in the recession all at once in 1929. It didn't! The stock market crashed in 1929, but GDP growth didn't reach it's low point and unemployment didn't reach it's high point until several years later, in the early 1930s. The fact that the crisis so far has been restricted to the housing market and the money market is no proof that "the rest of us are safe". This drop in auto sales is likely an opening salvo in a war on the "real economy" - and we're probably going to start to see other bad numbers trickle in.

The biggest recent news is that the crisis is spreading to Europe and Asia. This is also bad news in terms of the possibility of a broader recession. The only thing buoying us in the last year or so has been - ironically - our exports. If aggregate demand contracts in Europe and Asia, you can bet that component of GDP is going to drop and suddenly we're going to be looking at negative GDP growth - recession territory. Paul Krugman has a good, albeit brief post on the global nature of the crisis this morning. He specifically compares out situation to that of Brazil, Thailand, Indonesia, Russia, and South Korea - who crashed in 1997-1998, in part because of their high exposure international financial flows. These have increased in the U.S. dramatically since 1995 or so. Which begs the question - what is the end game here? I see two things that could potentially happen - first, we could close up and insulate ourselves from the world economy. It could also be a Bretton Woods moment - since we know that all this international connectivity exposes us to substantially more financial risk than in the past, it may be appropriate not just to reregulate our own financiers - but to establish a new international regulation of financial markets on the ruins of Bretton Woods. Not that we've been hearing any clamoring for this... and besides - who could possibly stand in for Keynes?

In election news... well, Obama is giving McCain a whooping for the most part. A few concerns - Palin is performing better than she has been (could she really be performing worse???), and McCain is on a smear hyper-campaign right now. I think it will make him look childish - but you never know. But overall I think it looks good. Michigan is a lock - Ohio, Pennsylvania, and Virginia are leaning Obama. Florida still sounds tough, but if Obama really gets all those swing states perhaps we could do without. I hear McCain and Obama are now heating up the war over Nebraska!... NEBRASKA! McCain is on the defensive in traditional red states. Not only does this not bode well for him in the red states, it means it's that much less resources he's going to spend in the blue states and the swing states - which is going to make keeping Michigan, Ohio, Pennsylvania, Virginia, etc. that much easier for Obama. Good news all around.

And... as I've been updating for months... Gilmore is a lost cause. Go Warner!!!

Monday, September 29, 2008

"A Day of Consequence"

{kind=link}

The House failed to pass the bipartisan bailout package this afternoon. While many Democrats voted against it and many Republicans voted for it, the majority of Republicans were opposed and the majority of the opposition were Republicans.

In response, the Dow Jones plunged 700 points, but has recovered somewhat since then.

Predictions of the ultimate effect of a failed bailout range from "just another recession" to a second Great Depression. At this point, these claims are hard to evaluate because the direness of the outcome depends on how the "ripple effect" play out (credit squeeze restricts business activity, which leads to layoffs, which leads to decline consumer demand, which restricts business activity further, which leads to more layoffs, etc.). Whatever happens, I hardly see how this could end up being a "normal" recession. I'm not convinced that it's going to be another Great Depression or even close to another Great Depression - but I haven't been convinced that it won't turn out that way either. Whatever happens, we are talking about the potential for substantial economic damage. I believe the failure of the House to pass this bill was reckless and irresponsible.

Steny Hoyer, representative from Maryland and the House Majority Leader closed the debate on this bill by saying that today was a "day of consequence". Now it's time to find out what those consequences are going to be.

Friday, September 26, 2008

McCain's Big Freeze

I was struck by McCain's supposedly "bold" budget proposal to freeze non-entitlement, non-defense program spending (entitlement programs are Social Security and Medicare - and some people include Medicaid in the count, but that's not as important because Medicaid isn't nearly as big as Social Security or Medicare). WOW! What a bold plan! Let's talk a little about this "bold plan"...

Social Security and Medicare are called "entitlement programs" because once you reach age 65 you have the right to claim them. Your age is your eligibility (of course in the case of Social Security you also have to have paid into it for a certain amount of time, but it is guaranteed to everyone that paid into it). Since these programs are guaranteed, and since people are living longer, healthier lives in the United States than they used to, spending growth in these programs has been tremendous since they began. The future growth in these programs is going to dwarf even the growth to date with the retirement of the baby-boomers.

Defense spending growth hasn't been quite as continuous as entitlement program spending; it went down significantly after the Cold War in the 1990's, but obviously it makes up a nice chunk of our budget now with the War on Terror and the Iraq War.

The other thing that's grown significantly for the last several decades has been interest payments on the national debt. That's right guys, we aren't just indebted to our East Asian creditors - we need to pay them interest on top of the principle just like any other debtor. So all though McCain didn't mention it, I'll throw interest payments in, because my guess is that either Obama or McCain would cut entitlements or defense before they stop paying the interest on our debt (the world has enough doubts about our solvency... don't want to cause any more jitters)!

So, when you take all that out of the budget you have two things: what the CBO calls "other mandatory spending," and "discretionary spending". Discretionary spending includes everything from good old fashioned "bridge to nowhere" pork, to child care subsidies, to the National Science Foundation budget. That's where McCain proposes the spending freeze.

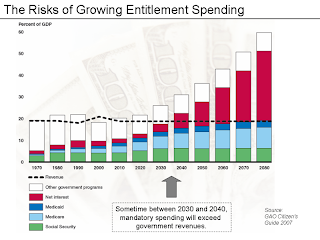

Unfortunately for McCain, he's not being as bold as he thinks he is! Non-defense, non-entitlement, non-interest payment spending has been essentially frozen for YEARS because growth in these programs has been crowded out by the growth in defense, entitlement, and interest spending! Take a look at the chart from the GAO, below, and you'll see what I mean:

Social Security and Medicare are called "entitlement programs" because once you reach age 65 you have the right to claim them. Your age is your eligibility (of course in the case of Social Security you also have to have paid into it for a certain amount of time, but it is guaranteed to everyone that paid into it). Since these programs are guaranteed, and since people are living longer, healthier lives in the United States than they used to, spending growth in these programs has been tremendous since they began. The future growth in these programs is going to dwarf even the growth to date with the retirement of the baby-boomers.

Defense spending growth hasn't been quite as continuous as entitlement program spending; it went down significantly after the Cold War in the 1990's, but obviously it makes up a nice chunk of our budget now with the War on Terror and the Iraq War.

The other thing that's grown significantly for the last several decades has been interest payments on the national debt. That's right guys, we aren't just indebted to our East Asian creditors - we need to pay them interest on top of the principle just like any other debtor. So all though McCain didn't mention it, I'll throw interest payments in, because my guess is that either Obama or McCain would cut entitlements or defense before they stop paying the interest on our debt (the world has enough doubts about our solvency... don't want to cause any more jitters)!

So, when you take all that out of the budget you have two things: what the CBO calls "other mandatory spending," and "discretionary spending". Discretionary spending includes everything from good old fashioned "bridge to nowhere" pork, to child care subsidies, to the National Science Foundation budget. That's where McCain proposes the spending freeze.

Unfortunately for McCain, he's not being as bold as he thinks he is! Non-defense, non-entitlement, non-interest payment spending has been essentially frozen for YEARS because growth in these programs has been crowded out by the growth in defense, entitlement, and interest spending! Take a look at the chart from the GAO, below, and you'll see what I mean:

OK - this is REALLY hard to see, I know - but the white bar at the top is non-entitlement spending (I believe it actually includes defense in this case!). The red, blue, and green bars are interest payments, Medicare, Medicaid, and Social Security. The dashed line is projected government revenues, and the scale for this is spending as a % of GDP. Terrible picture, I know - I tried to find a better one. But I think it illustrates my point: because of the growth in defense, entitlement, and interest spending there has been no growth in other spending anyway! The freeze is already here! In many programs, spending has actually declined already.

OK - this is REALLY hard to see, I know - but the white bar at the top is non-entitlement spending (I believe it actually includes defense in this case!). The red, blue, and green bars are interest payments, Medicare, Medicaid, and Social Security. The dashed line is projected government revenues, and the scale for this is spending as a % of GDP. Terrible picture, I know - I tried to find a better one. But I think it illustrates my point: because of the growth in defense, entitlement, and interest spending there has been no growth in other spending anyway! The freeze is already here! In many programs, spending has actually declined already.

The way to solve our long-term fiscal problem is to cut exactly what McCain proposes to let go: defense, entitlements, and interest... and we really don't have many options even there:

Defense: I'm not too excited about the prospect of cutting defense spending. Bringing a safe and responsible conclusion to the Iraq War will certainly save some money, but I agree with Obama that we're just going to have to move at least a portion of that war effort to Afghanistan. In addition, we need to reinvest in our equipment and defense infrastructure that has been worn down by Iraq, AND we need to provide a higher quality system to serve the veterans that will be returning. So I don't see much prospect of reducing defense spending, and I don't think anybody else does.

Interest: Talking about interest is easy. There are only two things to remember: first, we have to pay it - there's no choice involved. Second, the only way to reduce it is to reduce the debt. Period. [Not entirely true... we could always have our mints crank out currency which will reduce the value of our currency... then we can pay them back in worthless bills. But I don't think we want to go this route!]

Entitlements: The 800 pound gorilla in the room. The fact is, we need to cut entitlement spending or raise entitlement taxes. This isn't a debating point, it is quite simply the only way to regain fiscal responsibility. I've worked with Robert Reischauer, one of the biggest budget wonks out there, for the last two years and through him I've met lots of other big budget wonks. Doesn't matter what party they're associated with, they all agree - the solution to the budget problem is dealing with entitlement spending. Nobody owned up to this in the debate, which was telling about how hard it's going to be. Obama did mention one part of Medicare that could be cut - the Medicare Advantage "subsidy". Ever since 1997, Medicare beneficiaries have had the option of enrolling in privately administered Medicare plans, known as "Medicare Advantage". Fine - the idea was to harness the competitiveness of the private market... I can buy that. The problem is, the government ends up paying around 15% more for those plans than they do for "regular" Medicare plans. That's great - cutting that subsidy to the level of other Medicare plans and making beneficiaries pay the difference if they still want the private insurance sounds like a smart idea to me.

The problem is, even Obama didn't demand fundamental reform. I'm NOT an expert on entitlement programs, but even I could suggest:

- First and foremost, freezing physician payments which is one of the fastest growing components of Medicare.

- Raise the eligibility age for both programs

- Eliminate the FICA tax cap. I'm not sure exactly what it is now, but it's somewhere around $100,000. You have to pay something like 7.5% of your taxable income into Social Security up to $100,000 right now. After $100,000, your income isn't taxed!!! Why is this? This means that the rich actually pay a LOWER tax rate than the poor when it comes to Social Security! Now, I know there are legitimate ethical cases against a progressive income tax... but who in their right minds supports a REGRESSIVE tax??? Raising or eliminating this cap would help things out.

- Cut benefits. Yes - my specific suggestions and expertise end here, and I have to offer the non-descript "cut benefits". Someone more familiar with the program than I can get into the specifics.

We can do this - we need to have the strength to take on the entitlement programs. That will make substantially more difference than any pork-cutting programs that McCain and Obama propose. Nobody embraced this, although Obama made it clear that he was open to reducing some entitlements. I hope he's just holding his tongue because saying "I'm going to cut Social Security" would be the kiss of death on the campaign trail. Perhaps he'll be more energetic on this front than he lead on. But don't be fooled by that little discussion they had on the budget... McCain wasn't being bold at all - he was essentially describing the status quo. And Obama didn't offer a whole lot either.

Krugman's insights on the crisis...

I'm cutting and pasting a Paul Krugman post in it's entirety, because I think it's scary and insightful. I don't buy all his criticisms of Republicans, but nevertheless this is a good summary of the current impasse (which I would blame on Republicans... at least a faction of them):

"A few more thoughts about the incredible scene described in today’s Times (great reporting, by the way):

In the Roosevelt Room after the session, the Treasury secretary, Henry M. Paulson Jr., literally bent down on one knee as he pleaded with Nancy Pelosi, the House Speaker, not to “blow it up” by withdrawing her party’s support for the package over what Ms. Pelosi derided as a Republican betrayal.

How did we get to this point? It’s the culmination of many past betrayals. First of all, we have the Republican Study Committee blowing things up with a complete nonsense proposal — solving the crisis with a holiday on capital gains taxes. How is that possible? Well, if a party runs on economic nonsense for 25 years, eventually many of its foot soldiers will be people who actually believe the nonsense.

More specifically, though, the failure to get a deal reflects the betrayals of the Bush years. Democrats weren’t going to trust Henry Paulson, because behind him they see the ghost of Colin Powell (and Paulson’s “all your bailout are belong to me” proposal, aside from being bad economics, showed an incredible tone-deafness.)

And after the way the Bushies and their allies double-crossed the Democrats again and again in the aftermath of 9/11 — demand national unity, then accuse you of being soft on terrorists anyway — there’s no way Pelosi and Reed will do the responsible but unpopular thing unless the Republicans agree to share ownership.

So what we now have is non-functional government in the face of a major crisis, because Congress includes a quorum of crazies and nobody trusts the White House an inch.

As a friend said last night, we’ve become a banana republic with nukes."

"A few more thoughts about the incredible scene described in today’s Times (great reporting, by the way):

In the Roosevelt Room after the session, the Treasury secretary, Henry M. Paulson Jr., literally bent down on one knee as he pleaded with Nancy Pelosi, the House Speaker, not to “blow it up” by withdrawing her party’s support for the package over what Ms. Pelosi derided as a Republican betrayal.

“I didn’t know you were Catholic,” Ms. Pelosi said, a wry reference to Mr.

Paulson’s kneeling, according to someone who observed the exchange. She went on:

“It’s not me blowing this up, it’s the Republicans.”

Mr. Paulson sighed. “I know. I know.”

How did we get to this point? It’s the culmination of many past betrayals. First of all, we have the Republican Study Committee blowing things up with a complete nonsense proposal — solving the crisis with a holiday on capital gains taxes. How is that possible? Well, if a party runs on economic nonsense for 25 years, eventually many of its foot soldiers will be people who actually believe the nonsense.

More specifically, though, the failure to get a deal reflects the betrayals of the Bush years. Democrats weren’t going to trust Henry Paulson, because behind him they see the ghost of Colin Powell (and Paulson’s “all your bailout are belong to me” proposal, aside from being bad economics, showed an incredible tone-deafness.)

And after the way the Bushies and their allies double-crossed the Democrats again and again in the aftermath of 9/11 — demand national unity, then accuse you of being soft on terrorists anyway — there’s no way Pelosi and Reed will do the responsible but unpopular thing unless the Republicans agree to share ownership.

So what we now have is non-functional government in the face of a major crisis, because Congress includes a quorum of crazies and nobody trusts the White House an inch.

As a friend said last night, we’ve become a banana republic with nukes."

You have to choose...

The last two weeks, I've been frustrated with people (mostly Democrats, honestly) who insist that we have to punish Wall Street execs and help homeowners in this legislation. Steve Pearlstein of the Washington Post sums up my thoughts on this perfectly this morning:

The last two weeks, I've been frustrated with people (mostly Democrats, honestly) who insist that we have to punish Wall Street execs and help homeowners in this legislation. Steve Pearlstein of the Washington Post sums up my thoughts on this perfectly this morning:"You can try to prevent a financial meltdown or you can teach Wall Street a lesson, but you can't do both at the same time. So which will it be?"

We need to understand that there are two problems we're dealing with right now -

1. The first is that NOBODY is willing to lend money to anybody else, because they have no clue how much their assets are worth and they have no clue how reliable borrowers are. Wall Street is a deer caught in the headlights, unable to move right now - and when that happens money doesn't get pumped through our economy, with consequences potentially as disastrous as blood not pumping through the human body.

2. The second problem, of course, is the irresponsible lending habits of those Wall Street firms and the irresponsible borrowing habits of many American consumers that got us here in the first place. Contrary to popular belief, banks didn't "trick people" into getting mortgages they can't afford any more than homeowners tricked the banks into lending to them! Nobody tricked anybody and everybody cut corners.

The solution to the first problem is for the government to pump an unprecedented amount of money into the bloodstream of the American economy and do something to relieve fears of these "mortgage backed securities". The solution to the second problem is to withhold money from the economy and let the banks deal with their own mortgage backed securities and reap what they sow.

In other words, THE SOLUTIONS TO THE TWO PROBLEMS ARE DIAMETRICALLY OPPOSED TO EACH OTHER!!!! If House Republicans or sheepish Democrats want to focus on the second problem, we should just pass this legislation without them, because there is no way to achieve both objectives in the same piece of legislation.

That's not to say we should never deal with the second problem - we absolutely should. But the second problem has been with us for months now, and it will be with us for months even if we get through this current crisis. We need to deal with it later - through aid to homeowners, FBI investigations, greater regulation insuring transparency, etc... but LATER. For the time being, we should get rid of these so called "golden parachutes" to the extent that we can and lock up the big-time execs if they did anything illegal. But it makes no sense to make the banks themselves suffer at the same time that we try to help the banks. If you're a parent and your kid gets himself into a dangerous situation, the first thing you do is extract him from that dangerous situation, and only after he's safe do you light into him about how stupid it was to do that. Same principle applies here.

Obama has already shown an acknowledgement of this, which I like a lot. Part of the proposed legislation that Democrats were pushing for is to allow bankruptcy judges to renegotiate the terms of mortgages for homeowners going into default. The banking industry howled at that proposal, Democrats insisted on it... Obama said that it was absolutely inappropriate right now because the immediate problem is saving the banking industry, not tying their hands behind their backs.

Thursday, September 25, 2008

WWJMKD?

David Ignatius has a great article in the post on what Keynes would do to respond to the financial crisis. Of course, he doesn't give any specific Keynesian policy suggestions, but he does outline why considering issues of liquidity preference, animal spirits, and investor psychology trumps Friedmanesque quantity theory of money logic at a time like this.

To his analysis, I only want to add a quote from The General Theory itself:

"For my own part I am now somewhat skeptical of the success of a merely monetary policy directed towards influencing the rate of interest. I expect to see the State, which is in a position to calculate the marginal efficiency of capital goods on long views and on the basis of the general social advantage, taking an even greater responsibility for directly organizing investment; since it seems likely that the fluctuations in the market estimation of the marginal efficiency of different types of capital, calculated on the principles I have described above, will be too great to be offset by any practicable changes in the rate of interest."

To his analysis, I only want to add a quote from The General Theory itself:

"For my own part I am now somewhat skeptical of the success of a merely monetary policy directed towards influencing the rate of interest. I expect to see the State, which is in a position to calculate the marginal efficiency of capital goods on long views and on the basis of the general social advantage, taking an even greater responsibility for directly organizing investment; since it seems likely that the fluctuations in the market estimation of the marginal efficiency of different types of capital, calculated on the principles I have described above, will be too great to be offset by any practicable changes in the rate of interest."

Interestingly enough, one of Keynes's biggest champions today - Paul Krugman - has been quite skeptical this week about the state's ability to do exactly what Keynes thinks it can do - provide a better estimate of the "marginal efficiency of capital" than the market. I think Krugman's concerns have been overblown, though. He knows like everyone else that these assets are underpriced now. Krugman isn't worried that the state can't properly price the assets... he's worried that if they do properly price them they'll end up forking over a bunch of money to the banks with no strings attached.

Wednesday, September 24, 2008

McCain Transparency

It seems to me that all these things McCain has been pulling:

1. Outrage that Obama called Palin a "pig"

2. Accusing Obama of wanting to raise taxes on working Americans

3. Promoting Palin as someone who "said no to the bridge to nowhere"

and most recently...

4. Dumping Friday's debate to rush to Washington to deal with the financial crisis

are completely insincere and to me completely transparent. I understand that campaigns stretch the truth sometimes... Obama does that when he talks about McCain wanting to stay in Iraq "for 100 years". And there are other instances where McCain simply stretches the truth rather than promoting outright lies. But also prominent in the McCain campaign have been these instances where you just have to think "how can McCain SAY THAT and keep a straight face? There's no way even HE could believe that!"

Am I just being paranoid here? Am I just being cynical? Or is this stuff really as transparent as it appears to be to me?

Such a shame... I've always liked the guy, but there have been SO MANY cheap shots lately. I'm glad Obama said the debate should go on, and that he didn't just cave into McCain's ridiculousness.

Of course we need to work out a solution to this crisis... but that's not a free pass to get you out of a debate.

1. Outrage that Obama called Palin a "pig"

2. Accusing Obama of wanting to raise taxes on working Americans

3. Promoting Palin as someone who "said no to the bridge to nowhere"

and most recently...

4. Dumping Friday's debate to rush to Washington to deal with the financial crisis

are completely insincere and to me completely transparent. I understand that campaigns stretch the truth sometimes... Obama does that when he talks about McCain wanting to stay in Iraq "for 100 years". And there are other instances where McCain simply stretches the truth rather than promoting outright lies. But also prominent in the McCain campaign have been these instances where you just have to think "how can McCain SAY THAT and keep a straight face? There's no way even HE could believe that!"

Am I just being paranoid here? Am I just being cynical? Or is this stuff really as transparent as it appears to be to me?

Such a shame... I've always liked the guy, but there have been SO MANY cheap shots lately. I'm glad Obama said the debate should go on, and that he didn't just cave into McCain's ridiculousness.

Of course we need to work out a solution to this crisis... but that's not a free pass to get you out of a debate.

Alternatives to the $700B Paulson-Bernanke Fund

The Washington Post presents a good summary of other solutions to the Wall Street crisis that have been proposed by economists. This is refreshing. I've confessed my ignorance of what to do before on this blog, but I feel like I know enough to acknowledge a good proposal when I hear one - and I liked all of these (just couldn't come up with them myself!). I especially like the idea of an investment fund that the Post suggests. It's the most similar to the Bush plan, which the president should like. It can be a permanent fixture to help in future crises like this (and issue that Sen. Bayh made a big deal about in yesterday's Senate hearing), and it injects capital without letting banks off the hook for bad loans. Now, that of course opens the possibility that bank failures won't stop with this investment fund - but they should hurt the economy less (I believe that's the right way to think about it...).

In other news, I think Paul Krugman volunteered to be Obama's Treasury Secretary today... still a little hazy on that one.

A Washington Post-ABC poll gives Obama a 9 point lead among likely voters, but because of the Electoral College system, I'm not sure how that translates into his actual changes. The race remains close in several very important states.

One race that is not close is the Virginia Senate race, where Warner leads Gilmore by 30 points!

Sunday, September 21, 2008

Krugman on the bailout

I'm no finance economist, so in the last two weeks I've been left with reading what other experts have been writing, nodding my head "that sounds right," or shaking my head "that sounds wrong," without too much creative, original thought. I'll continue that tradition today and reference a good post by Paul Krugman - world renowned Princeton trade economist and regular New York Times colmunist.

My response to the bailout has been "yes - we need to put a stop to this cascade of bank failures" - but other than that I haven't really been able to comment intelligently. Krugman does a better job than that, so I'll let him enlighten you today.

My response to the bailout has been "yes - we need to put a stop to this cascade of bank failures" - but other than that I haven't really been able to comment intelligently. Krugman does a better job than that, so I'll let him enlighten you today.

Thursday, September 18, 2008

Negative Three Month Treasury Yield

The yield on a three month treasury bill went negative this morning. That means that people are paying the government to borrow their money. The price of gold is going through the roof because people are also willing to put their money there.

The good news: this means people still have confidence in the U.S. government, at least. They could be dropping Treasury bills for gold alone, after all.

The bad news: this means that every single other security out there is so bad that people are paying the institution they believe most reliable (the government) to take their money. People now feel like their optimal choice is taking a guaranteed loss. When the optimal is a negative return, that is not good.

I've personally been worried that when this whole Chinese-financed financial free-for-all finally burst, people would run like mad from a U.S. government that couldn't pay it's debts. Thankfully that hasn't happened yet. They're running toward the government. I guess that just goes to show that even when you've been fiscally irresponsible, having a defense budget that equals the rest of the world's combined and having the most advanced civilization in the history of the species still buys you something!

The good news: this means people still have confidence in the U.S. government, at least. They could be dropping Treasury bills for gold alone, after all.

The bad news: this means that every single other security out there is so bad that people are paying the institution they believe most reliable (the government) to take their money. People now feel like their optimal choice is taking a guaranteed loss. When the optimal is a negative return, that is not good.

I've personally been worried that when this whole Chinese-financed financial free-for-all finally burst, people would run like mad from a U.S. government that couldn't pay it's debts. Thankfully that hasn't happened yet. They're running toward the government. I guess that just goes to show that even when you've been fiscally irresponsible, having a defense budget that equals the rest of the world's combined and having the most advanced civilization in the history of the species still buys you something!

The Great Rebalancing

Steven Pearlstein has a good article in the Post this morning that presents a big-picture view of the financial crisis. He presents a very stark case - that this crisis is nothing less than the rebalancing of the global imbalances that have persistently defied economic gravity for at least the last two decades.

For years we have been willing recipients of a flood of cheap cash from abroad - mostly East Asia, but elsewhere as well. We didn't get this cash by exporting - we got it by borrowing it. The government borrowed it, corporations borrowed it, and through banks and credit card corporations, families borrowed it from places like Japan, Taiwan, and now China. That flood of money pushed up prices everywhere - price increases in real estate allowed the average American family to live a life of luxury they had never known before. Tuitions sky-rocketed, but record rates of college attendance were still attained because of the availability of student loans. Our government was able to wage indefensible and unconscionable wars because it didn't have to ask the American people for any kind of sacrifice. Why would they bother asking for that kind of sacrifice? The Chinese were more than willing to finance the invasion of sovereign nations!

In other words, for the last two decades bubbles have been percolating throughout America. Bubbles in housing. Bubbles in tech stocks. Bubbles in ALL stocks. Buyers were readily available to get a piece of the pie which seemed to magically keep increasing as East Asia pumped more and more cash into our economy. Then one bubble burst - housing. And another - investment banking. Now with the precarious state of the newly nationalized AIG, banks that American families interact with on a daily basis look more unstable.

Pearlstein uses scary language:

"You know you're in a heap of trouble when the lender of last resort suddenly runs out of money."

"What we are witnessing may be the greatest destruction of financial wealth that the world has ever seen -- paper losses measured in the trillions of dollars." (when he says "paper losses" here it sounds rather trivial... but remember how many jobs were created by those "paper gains").

"But more than psychology is involved here. What is really going on, at the most fundamental level, is that the United States is in the process of being forced by its foreign creditors to begin living within its means. "

I've talked at length about the danger of "global imbalances" in the past. Everybody that's written about them has prayed for a "smooth landing". And who knows - maybe we'll get a relatively smooth landing and this is just a really bad business cycle. Maybe by 2010 or so, foreigners will still want to lend to us... just less than they did before. I hope so.

One thing is for sure - with the events of the last three days, 2008 will enter the history books next to 1981, 1929, and 1873. It will be a doozy people - and unlike '81 and more like '29 and '73, '08 is likely to completely redraw the economic and power map in the United States and the world - we will spend differently, we will have different national priorities, we will interact differently with the rest of the world, and we will look at ourselves differently afterwards.

For years we have been willing recipients of a flood of cheap cash from abroad - mostly East Asia, but elsewhere as well. We didn't get this cash by exporting - we got it by borrowing it. The government borrowed it, corporations borrowed it, and through banks and credit card corporations, families borrowed it from places like Japan, Taiwan, and now China. That flood of money pushed up prices everywhere - price increases in real estate allowed the average American family to live a life of luxury they had never known before. Tuitions sky-rocketed, but record rates of college attendance were still attained because of the availability of student loans. Our government was able to wage indefensible and unconscionable wars because it didn't have to ask the American people for any kind of sacrifice. Why would they bother asking for that kind of sacrifice? The Chinese were more than willing to finance the invasion of sovereign nations!

In other words, for the last two decades bubbles have been percolating throughout America. Bubbles in housing. Bubbles in tech stocks. Bubbles in ALL stocks. Buyers were readily available to get a piece of the pie which seemed to magically keep increasing as East Asia pumped more and more cash into our economy. Then one bubble burst - housing. And another - investment banking. Now with the precarious state of the newly nationalized AIG, banks that American families interact with on a daily basis look more unstable.

Pearlstein uses scary language:

"You know you're in a heap of trouble when the lender of last resort suddenly runs out of money."

"What we are witnessing may be the greatest destruction of financial wealth that the world has ever seen -- paper losses measured in the trillions of dollars." (when he says "paper losses" here it sounds rather trivial... but remember how many jobs were created by those "paper gains").

"But more than psychology is involved here. What is really going on, at the most fundamental level, is that the United States is in the process of being forced by its foreign creditors to begin living within its means. "

I've talked at length about the danger of "global imbalances" in the past. Everybody that's written about them has prayed for a "smooth landing". And who knows - maybe we'll get a relatively smooth landing and this is just a really bad business cycle. Maybe by 2010 or so, foreigners will still want to lend to us... just less than they did before. I hope so.

One thing is for sure - with the events of the last three days, 2008 will enter the history books next to 1981, 1929, and 1873. It will be a doozy people - and unlike '81 and more like '29 and '73, '08 is likely to completely redraw the economic and power map in the United States and the world - we will spend differently, we will have different national priorities, we will interact differently with the rest of the world, and we will look at ourselves differently afterwards.

Wednesday, September 17, 2008

McCain and Hoover

Paul Krugman's blog has been very active lately. One of the things he's posted is this article from the American Prospect on the similarities between John McCain's statements about the economy being "fundamentally strong", and Herbert Hoover's similar pronouncements before the Great Depression.

An interesting thought - and I think the parallel is worth noting. McCain does sound quite out of touch on the economy these days, even when you disregard the comments of some of his staffers and just focus on what he says (i.e., "the nation of whiners" fiasco).

But at the same time, I have to give John McCain some credit here. I think the point is that most of the fundamentals of our economy are strong. We have strong, flexible labor markets, a great education system that provides one of the highest and broadest-based levels of human capital in the world, a reliable currency, a stable government, a wide consumer market, and a mobile population. We have a LOT going for us that will allow us to weather this current financial typhoon.

But one fundamental that is not strong is the stability of the investment banking industry. Robert Samuelson, as usual, provides some great insights in to these issues in this morning's Post. He describes how freely available capital, and poor regulation of the measurement of the amount of risk involved in these new securities has allowed investment banks to take unprecedentedly risky bets. That is one fundamental that is NOT strong... and even worse - not only is it not strong, but for years it has given the impression of strength where there was none.

So overall I'd say yes - McCain is the wrong choice if you're worried about the economy. But Krugman shouldn't overplay his cards. McCain is right that most of our economy is fundamentally strong, but wrong about it in the one instance that really matters this time - and is costing us hundreds of billions of dollars.

An interesting thought - and I think the parallel is worth noting. McCain does sound quite out of touch on the economy these days, even when you disregard the comments of some of his staffers and just focus on what he says (i.e., "the nation of whiners" fiasco).

But at the same time, I have to give John McCain some credit here. I think the point is that most of the fundamentals of our economy are strong. We have strong, flexible labor markets, a great education system that provides one of the highest and broadest-based levels of human capital in the world, a reliable currency, a stable government, a wide consumer market, and a mobile population. We have a LOT going for us that will allow us to weather this current financial typhoon.

But one fundamental that is not strong is the stability of the investment banking industry. Robert Samuelson, as usual, provides some great insights in to these issues in this morning's Post. He describes how freely available capital, and poor regulation of the measurement of the amount of risk involved in these new securities has allowed investment banks to take unprecedentedly risky bets. That is one fundamental that is NOT strong... and even worse - not only is it not strong, but for years it has given the impression of strength where there was none.

So overall I'd say yes - McCain is the wrong choice if you're worried about the economy. But Krugman shouldn't overplay his cards. McCain is right that most of our economy is fundamentally strong, but wrong about it in the one instance that really matters this time - and is costing us hundreds of billions of dollars.

Tuesday, September 16, 2008

Yes America, we pulled a Chavez...

So the federal government effectively nationalized the largest insurance company in the country. Oh wait, not the federal government... the federal reserve board... you know, that thing that operates independently of our elected officials, save the occassional appointment of a chairman.

I don't know if this is as scary or shocking as it sounds - but it does make me wonder. To quote the senior Senator from New York: "The administration is approaching an unprecedented step, but unfortunately we are living in unprecedented times".

I don't like unprecedented times... there's just not precedent for them!

I don't know if this is as scary or shocking as it sounds - but it does make me wonder. To quote the senior Senator from New York: "The administration is approaching an unprecedented step, but unfortunately we are living in unprecedented times".

I don't like unprecedented times... there's just not precedent for them!

***

Representative Barney Frank (D - MA) is proposing the creation of a new federal agency to buy bad debt and reorganize companies as a long-term solution to the crisis. This article notes that a similar action was taken during the S&L crisis of the 1980s, but the that goal there was much simpler - limit taxpayer liability. The government was on the hook to insure those deposits.

No such clear cut goal exists in this case - it's not clear whether Frank's agency would be charged with lowering taxpayer liability (i.e. - probably selling off our newly nationalized companies as quickly as possible so that we're not left holding the bag there), protecting large financial institutions, or protecting homeowners.

On the deposit insurance front - it looks like all this could expand beyond the investment banking industry. The same article I linked to above suggests that Washington Mutual may be in trouble - and that if the government were to bail them out (which they are obligated to do because it's a deposit institution), then it could deplete half of the FDIC fund.

Friday, September 12, 2008

Heckman on the econometrics of prayer and God

So I was trolling the IZA website for new working papers today and found a really interesting little paper by James Heckman - prolific Chicago economist.

It estimated (if I understand him right) the effect of prayer on God's attitude towards man, by assuming that prayer is an increasing function of God's attitude towards man. As the attitude becomes more positive, people pray more. You can derive God's attitude towards man as a function of prayer from this prayer function and the population distribution of prayer (as captured by survey data).

I'm still a little confused by how all this works, but Heckman is a smart guy. I'm sure his math is right, I'm just not sure what implicit assumptions he's making to make the math right.

But it does make me wonder - we've seen all kinds of studies about how "prayer makes people in hospitals heal faster" - but you don't see social scientists doing this much. You don't see anything on the effect of prayer on neighborhood crime, or income, etc. It would be an interesting exercise simply because of what it would take to identify an unbiased estimate. After all, conceivably you'll pray more if you have a higher inherent likelihood at having a rough go at things - so that should negatively bias the effect of prayer. You'd have to find some instrument or exclusion principle predicting prayer. But it could work and that would be an interesting thing to write about.

But even once you get the unbiased estimate you still have Weber's conundrum - did you really estimate that Providence was shining down on the faithful, or did you just pick up some normative or cultural artifact that is positively (but spuriously) correlated with the prayer itself. And again - simply the exercise of working through these possibilities would be interesting, but its doubtful you could come out with anything conclusive.

So why don't more economists do this? Why don't we look at the effect of prayer intensity in different metropolitan areas on the performance of sports teams? Or national religiosity and whether they're victorious in a war? Or just a simple "health and wealth gospel" look at the effect of religiosity on earnings. I'm sure we've had studies that say "religious people on average earn X more dollars than non-religious people", but that's a different endeavor from trying to identify an unbiased estimator for the causal effect of prayer.

And of course I forgot to mention - Heckman's results! He finds a positive effect of no prayer on God's attitude, with a negative effect of some but very little prayer, and a positive effect of a significant amount of prayer.

It estimated (if I understand him right) the effect of prayer on God's attitude towards man, by assuming that prayer is an increasing function of God's attitude towards man. As the attitude becomes more positive, people pray more. You can derive God's attitude towards man as a function of prayer from this prayer function and the population distribution of prayer (as captured by survey data).

I'm still a little confused by how all this works, but Heckman is a smart guy. I'm sure his math is right, I'm just not sure what implicit assumptions he's making to make the math right.

But it does make me wonder - we've seen all kinds of studies about how "prayer makes people in hospitals heal faster" - but you don't see social scientists doing this much. You don't see anything on the effect of prayer on neighborhood crime, or income, etc. It would be an interesting exercise simply because of what it would take to identify an unbiased estimate. After all, conceivably you'll pray more if you have a higher inherent likelihood at having a rough go at things - so that should negatively bias the effect of prayer. You'd have to find some instrument or exclusion principle predicting prayer. But it could work and that would be an interesting thing to write about.